If you have started researching the changes in Michigan’s auto insurance, the new auto insurance laws might make your head spin. Let us help you make sense of it. It sounds simple enough. Michigan has now lowered the requirement for PIP (personal injury protection) coverage to make your insurance more affordable. What has changed and what do these changes mean to you? The new law made sweeping changes to Michigan’s no-fault insurance. There will now be six levels of coverage instead of mandatory unlimited PIP coverage, but other changes go into effect in July as well. Because there were so many changes to Michigan’s auto insurance, it’s important that you talk with your agent about your coverage before the new PIP laws go into effect.

When do Michigan’s New Auto Insurance Laws Start?

On June 11, 2019 Michigan House Bill 4397 went into effect. The law, which starts July 1, 2020, contains major changes to Michigan’s no-fault insurance law. The new law removed the mandatory unlimited PIP coverage. Now Michigan drivers can choose between six levels of PIP coverage. There were several other changes introduced including a fee schedule for medical providers who care for individuals injured in an auto accident, changes in bodily injury and property damage (BI/PD) coverage, and a reduction in the fee charged by the MCCA (Michigan Catastrophic Claims Association).

Changes Starting July 1, 2020 – What you Need to Know?

Before you make changes to your policy you should talk to your insurance agent. Under the new law, your insurance agent is required to give you forms that describe the benefits and risks associated with your coverage options. The changes in the law start July 1, 2020 and apply to newly issued policies or policies renewed after July 1, 2020.

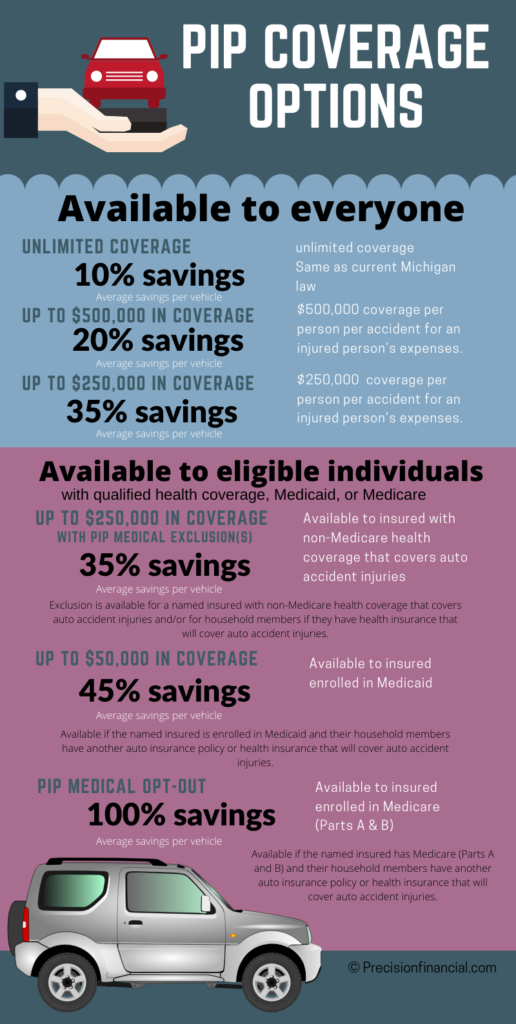

6 Levels of PIP Options

There are now six levels of PIP medical coverage for Michigan drivers to choose from. You can select the amount of coverage your auto insurance company will pay per person per accident.

- Unlimited coverage: Same as current Michigan law

- Up to $500,000 in coverage: $500,000 coverage per person per accident for an injured person’s expenses

- Up to $250,000 in coverage: $250,000 coverage per person per accident for an injured person’s expenses

- Up to $250,000 in coverage with PIP medical exclusion(s): Exclusion is available for a named insured with non-Medicare health coverage that covers auto accident injuries and/or for household members if they have health insurance that will cover auto accident injuries.

- Up to $50,000 in coverage: Available if the named insured is enrolled in Medicaid and their household members have another auto insurance policy or health insurance that will cover auto accident injuries.

- PIP medical opt-out: Available if the named insured has Medicare (Parts A and B) and their household members have another auto insurance policy or health insurance that will cover auto accident injuries.

Source: https://www.michigan.gov/autoinsurance

Temporary Reduction of Premiums

Michigan drivers will see a reduction in their auto insurance premiums. The new law requires auto insurance companies to reduce average PIP medical premiums for 8 years. Savings range from 10% to 100% on the PIP portion of your premiums. Keep in mind that the reduction is temporary and you are only saving on the PIP portion of your premium, which accounts for about a third of your total premium payment.

Changes to Liability Coverage

If you seriously injure another person in an accident, the injured party can sue you for damages. This is what the bodily injury coverage of your insurance policy is for. The current law limits damages to pain and suffering. Because all Michigan drivers were required to have unlimited PIP medical coverage, lawsuits to cover medical expenses were unlikely. After July 1, 2020 though, an injured person will be able to sue you for PIP expenses that their insurance doesn’t cover if they opted for a tier that is less than unlimited.

The new law increases the minimum bodily injury coverage your insurance company is required to offer you. Before July 1, 2020, the required amount of bodily injury coverage was $20,000 per person/$40,000 per accident. After July 1, 2020 the new default is $250,000 per person/$500,000 per accident. Drivers will have the option to reduce the amount of coverage to a minimum of $50,000 per person/$100,000 per accident.

Source: https://www.michigan.gov/autoinsurance

Reduction in Assessment Fee Charged by MCCA

The MCCA (Michigan Catastrophic Claims Association) is a non-profit association created by Michigan’s legislature. It provides unlimited lifetime coverage for medical expenses that are due to an auto accident. The MCCA reimburses auto insurance companies for each PIP medical claim in excess of $580,000. In order to finance the MCCA, all auto insurance companies are assessed a fee to cover the medical claims paid out by the MCAA. This is passed on to the consumer. Michigan drivers with unlimited PIP coverage currently pay a $220 assessment fee. The MCAA is reducing the assessment fee per vehicle to $100 beginning on July 2, 2020. The reduction will continue until June 30, 2021.

Fee Schedules

Health insurance providers and government insurance programs like Medicare and Medicaid use fee schedules to determine the price they will pay out for specific medical procedures such as an MRI. Auto insurers have not used a fee schedule, instead the law stated that they were required to pay whatever was “reasonable and customary.” Because of this, medical providers could bill auto insurers whatever price they deemed necessary. An MRI for an auto accident, for example, might cost an auto insurer $3,000, whereas Medicare only paid out $500 for the exact same procedure.

The new law establishes a fee schedule for medical providers who treat individuals injured in an auto accident. The fee schedule will limit providers to billing no more than 200-250% of what Medicare would pay for a medical procedure. The new reimbursement rates will be phased in starting on July 1, 2021.

Other Changes

- Requires agents to explain the benefits and risks of the coverage options you select. Your agent is required to give you forms to explain your coverage options.

- Eliminates non-driving factors such as sex, marital status, home ownership, educational level, occupation, and zip codes as factors in determining a driver’s auto insurance rates.

- Increases the amount that can be recovered in small claims court for uninsured damages.

- Creates a fraud investigation unit: The new fraud investigation unit will work with the Attorney General and law enforcement to investigate and prosecute insurance fraud.

- Requires prior approval: Auto insurance rates and policies must be filed and approved by the Department of Financial and Insurance Services before being offered to consumers.

- Increases fines on insurance companies, agencies and agents for certain violations of the law.

This is a brief overview of some of the 2020 changes in Michigan’s auto insurance laws. This is an overview only and it does not constitute legal advice. Please call us for help on explaining your coverage and selecting the right coverage for you.

*Important Disclaimer: This not intended as and does not constitute legal advice; instead, all information is for general informational purposes only. For legal advice on your auto insurance coverage please consult an attorney.

1 Comment

Add Comment